A story, in three parts.

First, what they’ve done going backwards, and what it lays the rhetorical groundwork to do in the future to help make things worse.

Second, what they’re doing going forwards to actively make things worse.

Third, a bird’s eye view of how much worse things were made.

Part 1: Loan Forgiveness Present

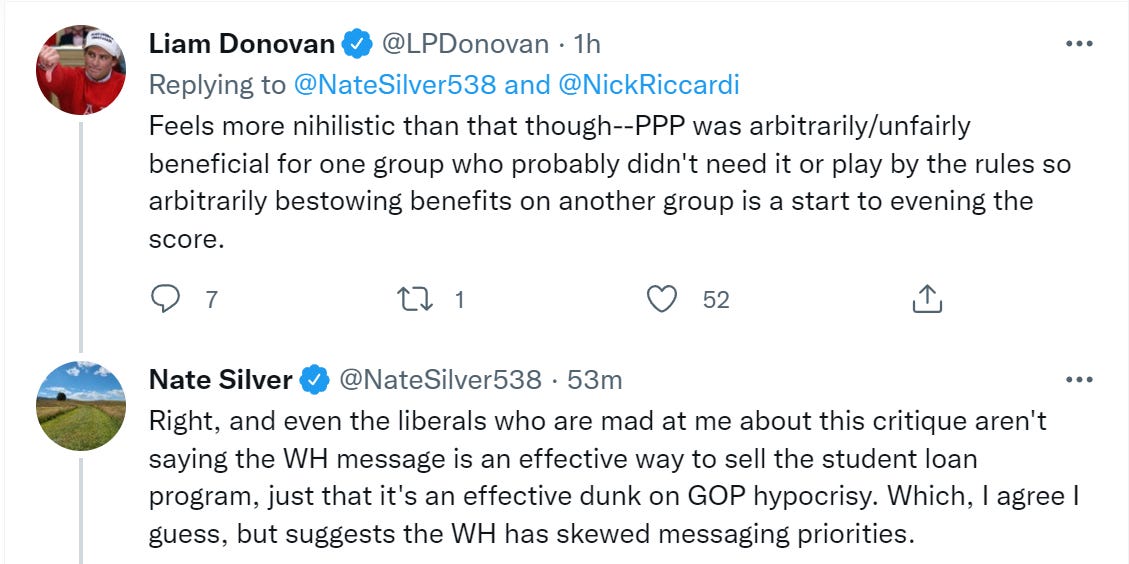

Those defending student loan cancellation are aggressively attacking anyone who disagrees with them, usually (but far from always) by pointing to their involvement in PPP – ‘This you?’

The implications are not great, including this obvious one.

This is indeed how I am interpreting the claim – that because the government once gave out a bunch of money to people, no one can ever object to giving other bunches of money to other people.

The argument flips freely between implying PPP was just and implying PPP was theft.

The White House is taking point on this.

I appreciate the brutal honesty here and also here:

A lot more than 51% of Twitter, and Democratic circles generally, approves of this.

The sky is blue. Also, the sky is blue.

It is far worse than this, because PPP loans were not functionally loans at all. They were grants for disaster relief, to be repaid if not spent, and when the government is handing out trillions it is rather expensive to simply turn down your allocated share. Drawing a parallel here implies that student loans were also ‘loans’ without intention of repayment. And any future loans are the same. There will be a scramble to take on and keep as much forgivable debt as possible, and things like tuition will adjust accordingly. The sky is the limit, the debtors’ revolt is complete, the treasury doors are open.

The response to this objection seems to be alternating between ‘the word loan is right there, checkmate (classical) liberals’ and ‘the outgroup’s words don’t have meaning so it is completely unfair to point out that ours also do not have meaning.’

If this general maneuver succeeds, it is also strong evidence that loan forgiveness, even fake ‘loan forgiveness’, leads to such spirals.

(Freddie DeBoer says the question of whether PPP was loans is irrelevant, what matters is the spending, except the whole point of the attacks is to say PPP ‘loans’ were loans and this justifies forgiving other loans. Back at the motte, he says this is a question of where the federal government spends money. He says PPP was justified by the need for ‘stimulus’ and this was a mistake because we overstimulated the economy, then seems to argue that this means we should overestimate it more because it’s fine to overstimulate, or something. And he explicitly says that because PPP wasn’t precisely targeted, that justifies precisely targeting a new group now and giving them money.)

More generally, assuming it deals with its other existential threats, Democracy survives until the public realizes it can vote itself money from the public purse in unlimited quantities. It is not hard to solve for the equilibrium.

Also more generally, the pattern of ‘launch personal attacks on everyone on the other side’ suddenly being the baseline argument does not exactly bode well. Nor does ‘force everyone to survive by accepting government funds then use this to attack anyone who objects to giving out more government funds.’ You should not (and cannot effectively in any case) sue over any of it, though.

There is also the widespread belief by those talking this way that they are helping to elect the candidates of the party they prefer. They think that no, this will not give their opponents a successful line of attack or make anyone all that angry. Intellectually, I know that they think this, and I even understand how they got there. It still boggles my brain every time.

Then again, perhaps they are right, and this will bribe voters (‘energize the base’) more than it enrages other voters. This is not an ‘explain the anger’ post such as this link, it is an analysis of what happened and what might happen next, and I am not the master of voter psychology.

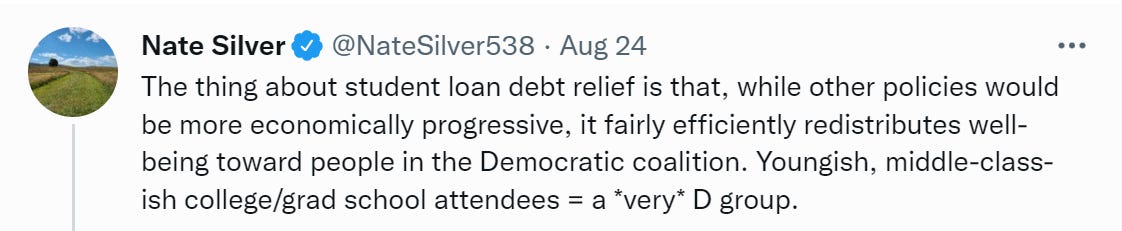

This post argues that loan forgiveness is not a gift to higher education but only to the students who get relief. The school already has the money. What does it care if the students are in debt or not in debt? The argument that this is not a one-shot game, and the possibility of cancellation was anticipated and is now more anticipated, is dismissed as not something students care much about and not the central thing. This does not seem right to me, but if students already don’t much think ahead to their debt repayments then the problem is already terrible but adding forgiveness makes it less worse.

The same dilemma will apply to the IDR modifications in Part 2 – if students don’t adjust their behavior based on prospective debt, then reducing their prospective debt does not change their behavior, which again means the changes do less marginal harm, but means that more marginal harm (especially to students) was already in the existing system. The resulting final system we have going forward (until it is fixed) is more, not less, broken.

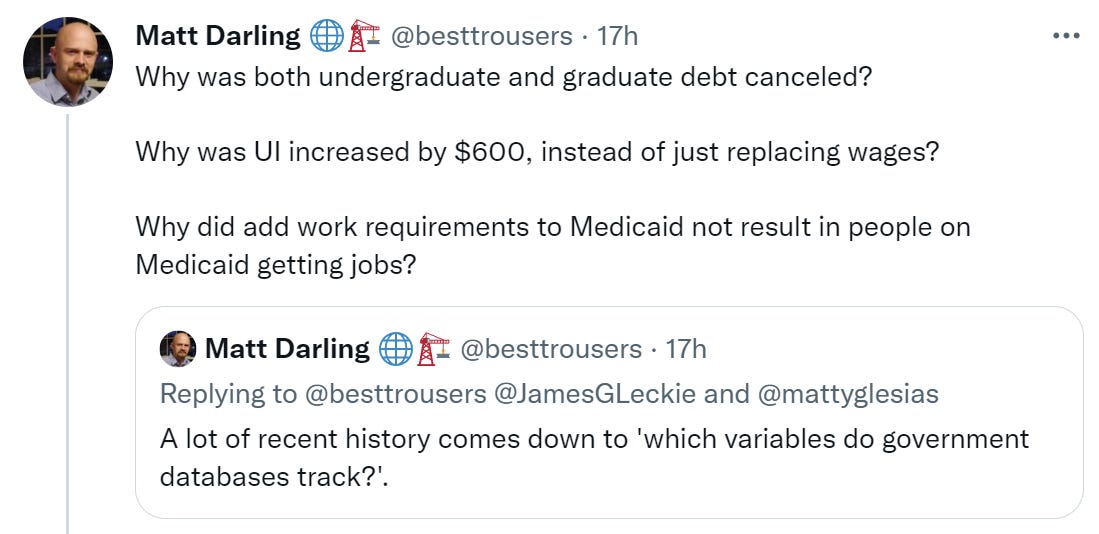

Another important point from Matt Darling is that graduate student debt was likely included in forgiveness because ‘college debt without graduate debt’ isn’t A Thing from the perspective of the administrative state. The system has no way to differentiate between the two.

A lot of the arguments for loan forgiveness, and policies that enable it, are a lot less absurd when confined only to undergraduate debt. It is for graduate debt where the whole thing goes over the top patently absurd.

Part 1a: Full Loan Forgiveness Implies Not Giving Out More Similar Loans, You Would Think

A note many have missed is that if you went to an especially terrible college then your entire loan is forgiven. Before I check or you check whether it is true, how many of them do you expect to still be taking students and offering loans?

Either at least these programs are frauds and/or utter failures, or they’re not.

If a single dollar of taxpayer money goes, at any point in the future, to subsidize the University of Phoenix, how is that anything other than pure theft?

I propose that if your program is so bad that any money borrowed to pay for it needs to be forgiven that, at a minimum, we do not offer any forms of federal loans, loan assistance or loan guarantees, or anything else that would enrich the program in question, to any future students of such programs, forever. If after this a student chooses to still go, it should be at their own risk and cost, full stop.

Ideally, of course, such places would all lose any and all accreditation. Alas, the government has outsourced accreditation. This would have suggested a simple solution to this problem, of course. If an institution loses accreditation, then loans would be forgiven. Which then creates a proper interest group to ensure it happens.

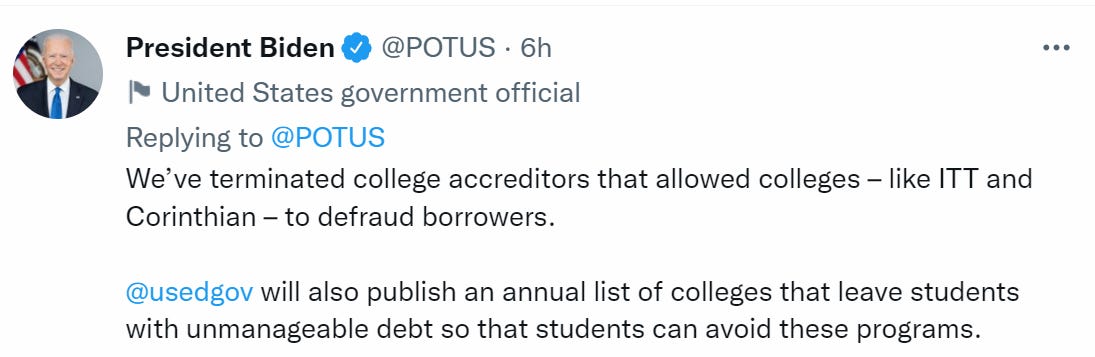

The president is taking at least some steps in this direction.

And yet I can’t help but notice that this should not count, not remotely, as ‘holding colleges accountable for jacking up costs without delivering value to students.’ Almost all colleges are doing this. We are ‘holding them accountable’ by forgiving student debt? And offering larger subsidies to future debt? I’d love to be ‘held accountable’ like that.

You know who got terminated? One of the accreditors. Not that they reliably used that accreditor, or that alternatives will be hard to find. That’ll show the bastards.

Part 2: Loan Forgiveness Future

And now for the second part: The Income Driven Repayment Program (IDR), along with the Public Service Loan Forgiveness Program, where Grand Theft Education potentially truly comes into its own.

From Matt Bruenig (Fortune Magazine also covers the issues here based on his post):

The IDR changes are four-fold:

Increase the amount of income not subject to IDR from 150 percent of the federal poverty line to 225 percent of the federal poverty line.

Eliminate any accrual of interest on IDR-enrolled loans.

For undergraduate debt, reduce the IDR rate from 10 percent of income beyond the threshold in (1) to 5 percent of income beyond the threshold in (1).

For IDR-enrolled debts with original loan balances below $12,000, reduce the repayment period from 20 years to 10 years.

…

Under the Public Service Loan Forgiveness (PSLF) program, law graduates that go on to work in the public sector, which is a lot of them as the public sector employs many lawyers, only have to pay 10 percent of their discretionary income for 10 years in order to have their debt forgiven.

Law schools figured out many years ago that, for a student who is planning to enroll in PSLF upon graduation, prices and debt loads don’t matter. Ten percent of your discretionary income is ten percent of your discretionary income regardless of what the law school charges you and how much debt you nominally have to take on.

Law schools also realized that they could make the deal even sweeter by setting up LRAPs [repayment programs, AT] that give graduates money to cover the modest repayments required by the PSLF.

The LRAP schemes work as follows:

The school increases their tuition.

The student takes out federal loans to cover the tuition increase.

The school squirrels away the debt-financed tuition increase into an LRAP fund.

The school disburses money from the LRAP fund to cover PSLF repayments.

Summarized:

Did you get that? Here’s a stylized example. Suppose a student will make 150k per year for 10 years working in the public sector. If they have 200k in debt they pay 15k every year to the government for 10 years and then 50k is “forgiven.” But now the law school comes to the student and says ‘heh, I have a deal which will make both of us better off. We are going to raise the price of law school to 400k but don’t worry not only won’t that cost you a penny more than the 15k a year you are already obligated to pay it will actually cost you much less because we will pay your payments of 15k per year!’ This indeed is a great deal for the student who pays nothing and it’s a great deal for the law school which gets 200k more revenue immediately in return for 150k of payments paid out over the following 10 years. Win-win! Except for the taxpayer of course.

(Note that legal salaries are bimodal, the job in question likely pays substantially below 150k.)

When I say Grand Theft, I mean Grand Theft.

I do think it is importantly less dire than this makes it sound. These are not true 0% interest loans. If they were, that would be completely insane – here’s someone gaming it out in real time. Fun stuff. Free money. Come get some.

Instead, this is (again, I think, we no longer are under Rule of Law here, the president thinks he has the power to snap his fingers and make things up so who can ever truly know in advance) a normal interest-bearing loan, except that if you fail to owe all the interest this month due to having insufficient income, they don’t tack the extra interest onto the loan – it cannot accrue.

That actually seems pretty fine, as long as the interest rate is adjusted accordingly and we do a good job collecting payments when they are owed. It makes it closer to a true income sharing agreement.

Not that I expect either of those conditions to hold, at least you tried cake, etc.

An interest rate, if substantial, at least puts some downside on the whole thing.

Without one, anyone who does not take advantage is a fool. Free money. Come get some.

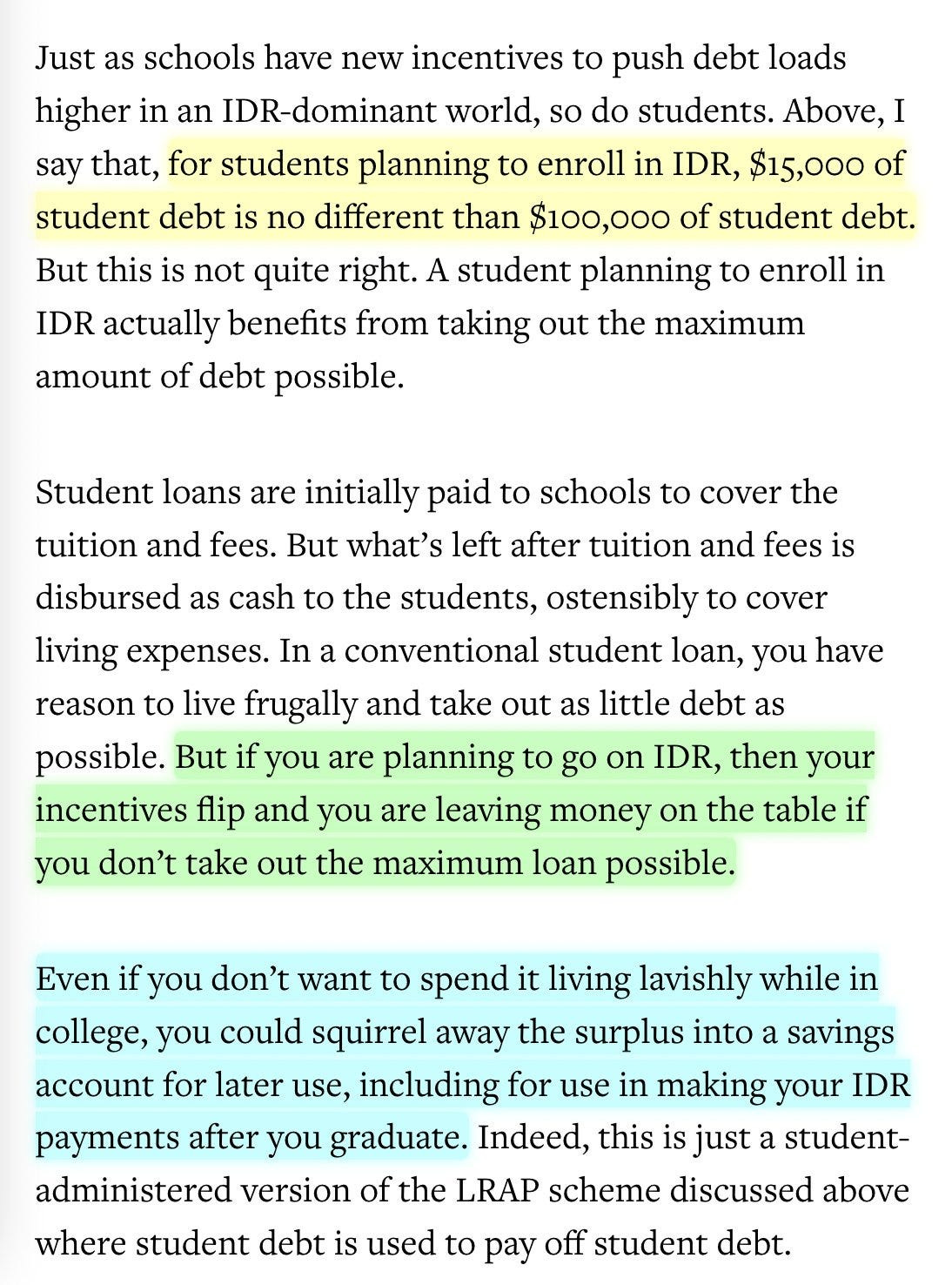

Notice that the percentage of income owed never changes, so the bigger the loan you take out, the smaller the percentage you’re likely to end up paying back before being ‘forgiven.’

This is still, if the understanding is correct, an open invitation to schools and students to take out the absolute maximum in Federal loans for every student. The more is borrowed, the larger the percentage that will ultimately be forgiven. Tuition is raised to match, and the profits shared between students and schools.

If, previously, a student was being offered need-based aid, but would have been instead eligible for Federal student loans, the school now has every incentive to insist upon student loans instead, even if this means covering all the payments. There is free money, and these are well-enough educated folk to realize this.

Also, as Matt Bruenig points out, a college student can and should (assuming some combination remotely sane interest rates and lack of expectation of truly huge amounts of future income) take out the maximum in loans regardless, since they do not need to be spent on tuition, invest the money, then use some of the money to pay back the loan and bank the rest as profit.

(One of the first two people to read a draft of this confirmed that they in fact did exactly this.)

I actively like the idea of true Income Sharing Agreements where you share a portion of your income, especially when offered by the school. Those are very good incentives. We pay for your education, you pay us based on your success. If you do not succeed, we don’t get paid. If you do succeed, you can end up paying a lot more than you borrowed, but you succeeded, so you can still come out far ahead.

The trick here is to make it a one-sided deal, and tack on loan forgiveness. You borrow a lot of money. If you don’t earn a lot, a lot of the loan gets forgiven, and also forget those pesky interest payments. Tons of free money. If you do earn a lot, it depends on the interest rate, but you’ve been making a lot of money, so you are not so unhappy you bought cheap insurance.

The other trick is that repayment amounts do not depend on loan size, at all, and forgiveness timing only has a threshold at $12k.Every dollar you borrow is a better deal than the dollar before. This is, of course, highly regressive. It seems completely crazy at the high end.

If I borrow $200k, does it make any sense that I only owe 5% of my discretionary income? Some quick math seems in order. Interest rates vary between 5% and 7.5%, so interest alone should be $10k/year minimum to start. Federal poverty line for an individual is $13,590, so 220% of that is $30k. To pay even the interest on the loan you would need to make $230k/year. To pay off the loan within 20 years you would need to be making more like $400k/year over 20 years. The average doctor, in 2019, made $300k.

This is not a loan. It’s a grant. You didn’t steal the money. We gave it to you.

So, yes. Going forward it really is like PPP.

The extension of all this to PSLF rewards students even more than before for going into public sector jobs. Thus at least part of this seems to go something like:

Take out loans.

Take a public sector job.

That requires a college degree.

Get loans forgiven after 10 years (instead of 20).

Instead of the job paying more money?

Thus, this could perhaps be best thought about as a raise in pay for public sector workers in their first ten years combined with a hike in tuition, with extra steps. Such workers save 5% of their discretionary income for 10 years. The average federal employee makes $108k/year, so this saves them about $50k.

Note that right now this program is quite tiny, only $290 million through the end of 2020. A lot of this is only 6.7% of those eligible applied for it, and also a lot of applications are pending or got rejected for bad paperwork. There’s a lot of room for this to grow, and with benefits scaled up presumably more people will take advantage.

In any case, why the extra steps?

Increase reliance on Federal government largesse and patronage.

Stick it to the other college students who pay higher tuition.

Make sure no one who doesn’t need loans goes into public service.

End run around unions to move pay down the seniority gradient.

You get to spend money without Congressional approval or paying for it.

Or people noticing what is happening.

Which is good, since most people would rather tuition be lower, not higher.

And they’d prefer the government give away less money, not more.

But hey, their fault. Should have studied harder in college.

What do you mean, a lot of people don’t go to college?

I do expect this obfuscation to largely succeed, in the sense that the theft will be sufficiently disguised to mitigate much of the outrage that would have otherwise occurred. Not all, by any means, but quite a lot. Which means this may be politically smart, if they didn’t succeed too well and have the beneficiaries also not notice, as an estimate below implies is likely.

Part 3: How Bad Is This Going To Get?

I mean, it’s not good, but magnitude is always tricky. So is the counterfactual, and so are the implications for future rhetoric and policy and culture and norms. We need to both estimate the true direct cost and the indirect costs.

I’ve laid out some of that above, but it’s time to put it together.

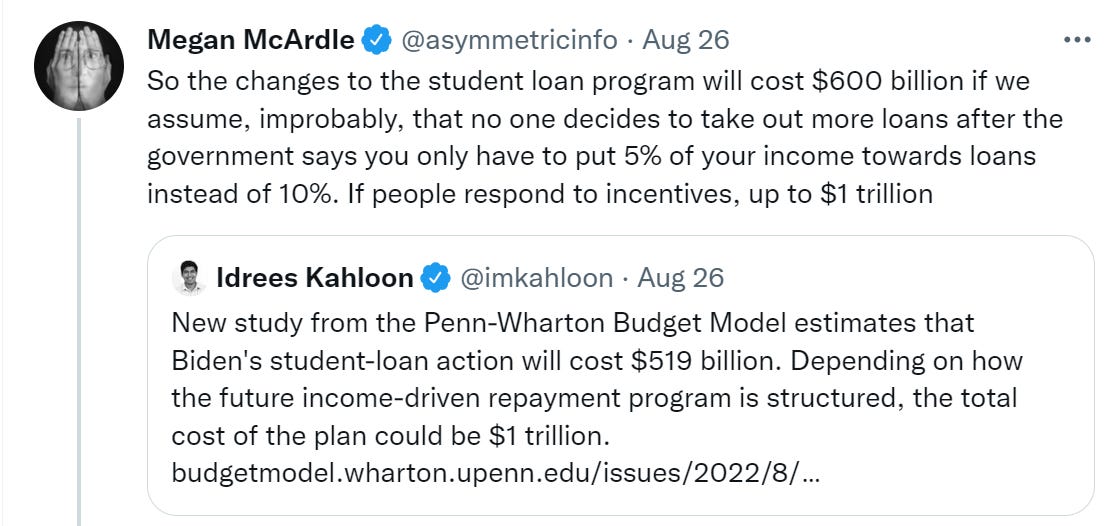

What will the final bill be? (direct link)

Summary: President Biden’s new student loan forgiveness plan includes three major components. We estimate that debt cancellation alone will cost up to $519 billion, with about 75% of the benefit accruing to households making $88,000 or less. Loan forbearance will cost another $16 billion. The new income-driven repayment (IDR) program would cost another $70 billion, increasing the total plan cost to $605 billion under strict “static” assumptions. However, depending on future IDR program details to be released and potential behavioral (i.e., “non-static”) changes, total plan costs could exceed $1 trillion.

As usual, this is scored over a 10-year window, because no one can envision a real future so the world always ends after 10 years. The bulk of the cost from loan forgiveness (part 1) is right away but then it starts going up again. The new IDR program (part 2) slowly grows over time, so with a ~5% discount rate but a >5% growth rate per year the technical long-term cost is limitless.

This analysis caps the cost of the IDR plan at $70 billion over 10 years by assuming that most people won’t take advantage of it because they won’t know to do so.

The new features in the new IDR proposal, however, could sharply increase take-up rates. Even many borrowers who anticipate not being qualified in future years would typically be better off enrolling in the intermediate years in which they are qualified. There would also be financial incentives for future borrowers to shift education financing toward more borrowing to take advantage of the 5% repayment threshold. If the Department of Education simply auto-enrolled borrowers for which it had sufficient information (i.e., switched from “opt in” to “opt out”), the additional costs of the IDR program alone could reasonably exceed $450 billion.

Thus, the $70 billion assumes ~15% uptake among the eligible. It also does not factor in any behavioral adjustment. The sky is potentially the limit here.

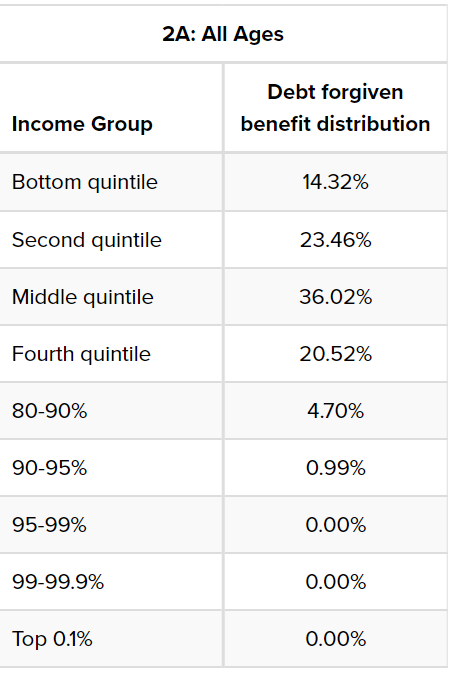

How regressive or progressive is all this?

By current income it is slightly progressive.

If current income is this close, by future income it is doubtless regressive, since those who have loans will have higher incomes in the future relative to now than those who do not have loans.

Also note that in general, whenever a program requires people to know to take advantage of complex stuff like IDR, the well-off tend to take advantage more often.

Thus, the final direct cost of these changes is somewhere between ~$600 billion and north of $1 trillion, depending on how much behavioral adjustment we expect and the extent to which we allow a lot of people to fail to enroll in the IDR program. With extensive IDR adjustments, it could get even bigger than that.

How big could it get going forward? The biggest-cost scenario is that IDR gets automatically applied to all loans. I keep trying to find flow estimates and getting stock estimates for everything, which makes estimation tricky. Then you have to factor in behavior and tuition adjustments. I am guessing that ~250 billion of loans get started every year right now, of which ~100 billion is graduate level and would mostly not be paid back, whereas the undergraduate debt that stays reasonably sized would be more of a mixed bag on getting repaid – if you borrow the average of $30k you only owe ~$1500 in interest per year, so past about $50k you start repaying, and average college graduate makes $68k, so they’d pay $900 principal a year to start, which is close to paying it back in 20 years, but the bigger loans are going to have big issues and some people won’t pay anything back at all even on smaller loans. And anyone going into public service is going to get a lot of forgiveness.

This then needs to be compared against the amount of forgiveness and non-payment that previously existed, since that doesn’t represent the situation getting any worse.

And then, you need to adjust for all the increases in tuition and loan size as a result of the changed incentives. All of this on, currently, something like (order of magnitude estimate only because Google wasn’t making it easy) $100 billion/year in graduate loans and $150 billion/year in undergraduate loans.

So, yes, this could all get very expensive, if we assume half or more of that is going to get ultimately forgiven, every year, forever. While getting bigger faster than inflation, every year, forever. Of course, when something can’t go on forever, it won’t.

That still excludes additional policy responses. How should we think about that?

The pessimistic case here is spelled out in Part 1 above. When you spend a bunch of money from the public purse to buy off your supporters, a logical consequence is that you justify and raise expectations for future buyoffs of supporters out of the public purse. People treat those who do not seek to become favored insiders and steal from the treasury as suckers, and both sides justify their bad behavior by pointing to past bad behavior. Loans are given out and prices charged based on the expectation that they can be used as leverage to steal from the public purse.

The optimistic case is that there may be a limited amount of low hanging fruit, a limited amount of money available to be stolen from the public purse, a limited amount of tolerance for such theft, and/or a subsequent demand for fundamental reforms.

My analysis of the Inflation Reduction Act found it to largely be picking low hanging fruit and using up limited capacities. Yes, several provisions were designed poorly or were ill-conceived, and would make things worse. The compensation is that it included a bunch of ways to save money, both in reality and as measured by the CBO, while only spending some of that money. The remaining savings were banked and will be hard to reclaim. Finding additional ways to record accounting savings, or find actual savings, will be more difficult, especially politically. Political capital was spent and ‘something was done,’ without that something being worse.

Could a similar case be made here?

Biden promised loan forgiveness during the campaign. He has now delivered loan forgiveness. It was larger than was strictly promised, as it includes IDR generosity and expansion, increasing Pell Grant forgiveness to $20k, and full forgiveness for victims of predatory programs.

Their plan to do anything about those predatory programsseems to be confined to revoke the authority of ACICS as an accreditor. My spot check of two places showed they were using the Higher Learning Commission, so I doubt this change will have much effect. WTF?

In exchange, payments on student loans are set to resume within a few months. The pandemic has effectively been over for a while and that rule kept going, so this was by no means a given. There were worlds in which student loan forgiveness didn’t happen, but all payments and interest stayed paused for another two years or more, and that could end up vastly more expensive as well as vastly more regressive.

Thus, there were arguments about whether to measure against ‘current law’ or some reasonable expectation of potential future law, such as expecting all temporary government programs to be permanent, since there is nothing so permanent as a temporary government program.

One could interpret the resumption as saying ‘all right, that’s enough, you’ve gotten your gift from the public purse and we’re done now.’ That doesn’t fix the system or anything, but perhaps it does buy some time.

We did not do anything to fix the broken system, yet we did acknowledge that it is broken. There is little argument there. We highlighted this, and used it as justification to spend quite a lot of money. That should strengthen calls to reform, even if doing it at the same time was a missed opportunity, perhaps?

Another parallel is the PPP ‘loan’ ‘forgiveness’ being vilified. This can end up going either way. On the one hand, the nightmare scenario laid out in Part 1, where any further thefts are considered justified by past thefts. On the other hand, perhaps this immunizes us so we can defend against future thefts, because we’re all so sick of them?

Consider TARP. TARP was very unpopular (although this was largely due to being seen as a far bigger giveaway than it actually was in expectation, and in the end the program made money in our particular Everett branch). Elected officials paid a political price to ensure it would pass anyway, to avoid what they feared (I believe quite correctly) would be an economic collapse if they hadn’t done it. One possible result would be that now it could have encouraged lots of moral hazard and giveaways to big banks. Another is that it could have used up the public’s tolerance for such measures, making a future TARP much harder rather than easier. That it would cause a crackdown on potential moral hazard rather than encourage more.

Given how we reacted to Covid, with bailouts and giveaways aplenty, one could reasonably say we very much did not learn our lesson. But circumstances were very different that time, on many levels. If we had needed something close to TARP 2, rather than a bailout aimed at what people like to call Main Street, would we have been able to do it? My guess is no, with potentially disastrous results. I do think the reaction here was protective rather than enabling. A counter response is that the Fed did a bunch of asset buying and market interventions that at least rhymed, so it’s not clear cut, but I do think we ended up in a reasonable place.

What about the impact on inflation?

When it comes to inflation of the true cost of higher education, ‘Not Great, Bob.’

That’s the answer when you include the costs borne by the Federal Government. The quantity of loans will rise, aid will shift into loans, and the sticker price will rise. The people, collectively, will have a bigger tab to pay.

However, what happens to the effective price paid if we look only at what future students will pay, and we assume they get to not pay the majority of their loans?

From the perspective of the student only, a loan that is a grant is no different from a grant. A loan that only gets paid back when the student makes lots of money is still a lot like a grant. Loan money that was already expected is forgiven more, so that’s a pure win. Tuition will go up, but tuition will presumably go up by less than the increase in loans taken out. So for the average student, it does look like they will be better off.

It’s not an efficient way to help students pay for college, because of all the additional money that will be seized by universities via tuition, a lot of which then will get spent in various unproductive ways, much of it in pure paying more money for the same things as before. There are ways to make the price paid cheaper without this effect (or without as much of this effect) but they involve something other than restricting supply and/or subsidizing demand.

What about inflation overall? What effect will this have? To some extent, humans are able to adjust their consumption based on anticipated future resources, so forgiving money owed in the future leads to more consumption now and thus to more inflation.

The flip side of this is that those with student debt are often importantly liquidity constrained, and lack the ability to borrow new funds on similar terms to the loans that were forgiven. Repayments have been paused for a while and will restart soon. The federal debt will increase, but it will take a while before this forces the printing of more money. I do think this will all combine to blunt the inflation effects somewhat, at least in the short term, and less consumption will be shifted than the headline costs would imply.

Finally, what effect will this have on tendency to steal in the future from the public purse? That is the hardest question to answer, especially in magnitude. I presume that it makes it easier, but considerations do, as noted above, go both ways.

Getting permanent modifications to the system in at the same time that were a further giveaway that made the problem worse, rather than waiting, was smart provided the changes were deemed necessary.

If and when Democrats try to ‘go back to the well’ a second time on student loan forgiveness, it would become impossible to continue pretending student loans were mostly loans rather than mostly grants. What kind of fool repays their grants? What kind of fool doesn’t apply for as many as they can get, or design their service to help others so apply?

Remember that originally there was pressure to do $50,000 per borrower. I am predicting that doing $10,000 now, then $40,000 later, would be harder than doing $50,000 up front, unless it is clear that theft is simply a political winner so it pays to do as much theft as possible, and the floodgates fully open.

Whereas I do think this makes further theft of other types easier, for both sides. If and when Republicans find a way to steal (ahem, ‘transfer money’) from blue voters to red voters, objections will be that much easier to laugh off. One possibility is that they will do this by going after higher education.

What Could Be Done Now?

I am exploring this and many other policy problems. As you would expect, it is hard. None of this is meant to imply I have a great solution to the problems in the cost and expansion of higher education, let alone issues with its content.

I can still brainstorm, so it seems like a good time to do that.

Signaling games and job requirements force our children to spend ever longer, and ever more money, on college. College is a positional good and students don’t feel its cost so schools largely compete on prestige and student appeal rather than price even before the student loan fiasco. Then the fiasco makes sure they really see all these prices as fake, and also makes them actually fake, so they keep going up, and life starts later and later and in more and more debt, so that everyone can stay where they would have been anyway.

(The exception is that cutting off loans, or at least loan assistance, to places where we are giving full forgiveness, is a pretty damn easy call. Not everything is hard.)

The solution starts with distinguishing costs from benefits. Going to college is not a benefit to society. It is a cost to society, which we subsidize and which prevents you from doing other things like working or starting a family. The benefit is if you get a useful education. Allowing students to signal via their education forces others to signal in expensive ways to keep up, whereas in a different equilibrium this would be a lot cheaper, so it is mostly a cost but it is important not to double count that cost.

We should not be trying to get every student into the most prestigious school for as long as possible, even at high cost, even when this drives a different student out because of lack of space. That is not helping.

Nor is providing additional subsidies to universities via student loans. Students cannot be charged more than they can afford to pay and can take out in loans. More loans encourage more price discrimination, allowing the universities to extract more money for the same product, or offer a luxury product students wouldn’t want to pay the marginal costs for in order to increase the university’s positional prestige.

The loan is helping the individual but each loan is a cost to society that makes things worse. The more subsidized the loan, the worse it makes things. Thus, the logical thing to do is to stop the Federal government from originating or subsidizing student loans going forwards, and allow any future student loans from other sources to be subject to ordinary bankruptcy proceedings at least after 5-10 years, and shift the administration of all grant programs to the university level to avoid bad incentives. Tuition will drop, grants and need based aid will replace many loans, and students will be better off overall.

If we think tuition would still be too high, we can offer per-student tuition aid across the board that reduces in size as tuition rises past a reasonable level, so raising sticker prices reduces the local pie size rather than increasing it.

Or we could, you know, cap the price of tuition outright, if schools want to benefit from the IDR program or student loans at all, or any of the other things we can condition on. In general price controls are terrible, but when the customer is not paying and the good is this positional I am willing to make an exception.

Would all this be regressive on the margin? This is unclear because among college students it is, but transfers from those who don’t go to college to those who do are highly regressive. My guess is it is net progressive. If that’s not good enough, it would be very easy to fix by taking some or all of the savings from not subsidizing loans and using it for a progressive tax cut. If necessary we can flat out make the tax code more progressive. When a child goes to college seems like a very odd time for a radical tax increase on families and their wealth. I presume we can do better than that. Reducing various educational job requirements, and some combination of restricting the requirement of an unnecessary college or graduate degree with easing restrictions on alternative ways to show you are the right one for the job, would also be a big help.

Would this reduce resources given to universities? Yes if we don’t compensate for it sufficiently, but it is not as if they use their resources on the margin to help students, or increase diversity, or lower tuition, or enroll more low income students. Again, they use it to compete. I do not see the value in that.

Again, take this section the least seriously in its details. The point is that the current system is deeply screwed up, is steadily inflating costs and driving everyone into debt and making them dependent on the whims of those who ‘forgive debt’ and what mechanisms lead to that. It isn’t the best possible solution, but if we basically scrapped the whole student loan system going forwards, we could reduce real total spending on higher education without sacrificing quality, and also not leave future children drowning in quantum debt.

In conclusion: It could be worse, we have paths forward available, and there is at least some upside to all this.

(As a datapoint, I am sufficiently out of the political loop that this post is incomprehensible to me e.g. this post assumes I know what ‘PPP’ refers to.)

PPP was a COVID program, intended to encourage companies to stay in business/employing workers by giving them money. (Name stands for ‘Paycheck Protection Program’.)

For years now, it has seemed to me that one of the root problems with all this is that the control loop is open: there’s effectively no feedback controlling loan amounts or who gets granted a loan.

If I could make only one single change in this system, I would allow student loans to be discharged like any other normal debt in bankruptcy. IMO, that was the single biggest class of mistake in this entire affair, as it removed the only ‘last resort’ superpower that loan takers had.

I would like to note that the naive version of this is bad. First, the naive version falls prey to new grads (who generally have nothing) declaring bankruptcy immediately after graduation. Then, lenders are forced to ask for collateral, which gets rid of a GREAT quality our current system has—you can go to college even if your parents weren’t frugal, no matter their income. I think this criticism probably still lands with a 5 year time horizon, maybe less for a 10 year.

I like the concept that lenders would take an interest in which major you were getting, since that seems like something that could use an actuarial table. I think we would benefit from more directly incentivizing STEM (and other profitable) degrees, which IDR doesn’t seem to do. What if IDR left lenders holding the bag?

Yes, the naive version of this is bad; but the point of a change like this isn’t that the immediate downstream effects are bad. The point is that the system as a whole is a giant adaptive object, and a critical part of the control loop is open. Closing the control loop has far, far more impact than just the naive version.

Consider cause and effect down the timeline:

Students are allowed to default, and start defaulting.

Loan companies change behavior, both to work with existing loan holders (so they don’t default) and be more selective about who they give loans to.

Loans become more likely for careers / degrees which have the ability to make money (STEM and friends), less likely for other degrees.

Number of students, and amount of money coming in to universities, drops.

Universities actually experience price pressure. They start cost cutting and dropping less useful things, and start shifting resources to degree programs with the most students.

Cost of a university degree slowly drops over time due to reduced demand and reduced funding.

Over time, there are broader societal shifts to deemphasize the idea that “everyone needs a degree”. Trade and other schools gain more prominence.

Universities start experiencing increased competitive pressure with trade schools.

… and other effects. Also, this is iterative—all of these components take time to respond and adjust to the new equilibrium, after which they will need to re-adapt.

Yes, it’s not a perfect solution, and yes, there’s definitely the concern that poor / disadvantaged students will have more trouble getting loans. But compensating somewhat for this would be the price drop, additional emphasis on trade schools, and deemphasis on needing a degree for any and all jobs.

Another expected objection might be, “with all these possible changes, how do we know this will be better?” To that I would answer: because we know the system is at least partially broken because the control loop on it is open. Any adaptive system with an open control loop is going to produce garbage; the first most obvious thing to do is to fix that.

Some meta questions I’m curious about:

Every president has an incentive to exploit existing laws to hand money to his or her supporters. Is Biden more egregious than usual, and if so why? (Personal reasons? Structural reasons?)

Biden is exploiting a provision in the law that says that the Secretary of Education can modify the student loan program in order to deal with emergencies (which just means whatever the President declares as an emergency). Is there any way to make this kind of provision less exploitable in the future?

Hey, for once planning only 10 years out maybe makes sense 😰 😅

I wonder if someone were to form a credible educational institution that used income sharing agreements in lieu of various loans, whether it could directly out-compete the current university system.

Actually making a creditable educational institution is a pretty big hurdle. I doubt the funding arrangement matters that much, and certainly I wouldn’t want to compete against the current system of loans you probably won’t have to pay back.

As far as I understand there’s a Supreme Court that isn’t friendly to increased government spending. The US constitution gives congress the authority to determine the budget and as a layperson this seems to me like a clear violation.

These debates seem to assume that the Supreme Court does nothing. Why is that assumption made?

This seems to be the official legal argument:

https://www.justice.gov/sites/default/files/opinions/attachments/2022/08/24/2022-08-24-heroes-act.pdf

So the argument seems to be that the Secretary of Education (who works for the President and will likely do whatever they’re told to do) was given the authority to “waive statutory and regulatory obligations for borrowers residing or working in a disaster area in connection with a national emergency and for borrowers who suffered economic hardship as a result of a national emergency”, everyone* suffered economic hardship as a result of COVID, and waiving entire debts is one way of waiving obligations.

I think you’re right that there’s a good chance the Supreme Court won’t allow this. Theoretically, Congress isn’t supposed to delegate the authority make laws or spend money, but the Supreme Court usually allows it.. up to a point. Spending half a trillion dollars on to protect people from the impact of COVID… in mid-2022.. seems like it might be too far for the Supreme Court. Not to mention that the current Supreme Court is probably not super impressed by an obvious attempt to bribe Democrats.

This isn’t spending per se; rather it is increasing costs. Any increase in spending happens in the course of existing programs, such as handing out more loans once students respond to the incentives.

On top of this, the federal financial structure is a unique and horrifying house of cards. Their accounting methods are actually unique to them, and sometimes vary by department or agency; auditing is difficult and inconsistent; much of it is seemingly designed to obfuscate, though in a change-the-standards-by-committee-to-make-us-look-less-bad way rather than an intelligence/defense sort of way.

Since most of what the President is doing is changing how existing programs and agencies operate, these maneuvers would be difficult to challenge. If any particular move is challenged, it can almost certainly be accomplished in a different way on firmer authority grounds. Meanwhile, someone has to bear the publicity burden of trying to ensure student debt never goes down to push the case all the way to the Supreme Court, which is a long and expensive task.

All of this assuming the Supreme Court would even hear such a case. This is one of those things that is difficult to bring before them due to the rules about standing, which is to say whether there is anyone suitable to bring the suit. The simplified version is that the person who sues has to have been harmed; but how to establish the harm to a person from someone else having debt forgiven or restructured?

Yeah, you’d have to prove that the costs are somehow shifted. That’s not at all clear. A dollar in accounts receivable is something of a legal fiction. It exists on a probability distribution according to how likely it is that the debt is going to be collected. Before credit cards, it was standard practice for businesses to “age” their AR over the course of months, ultimately writing off the most intractable debts. In many ways, that’s all that’s going on here. Credit cards are simply a way for businesses to sell their AR (at a modest discount). Interest rates partially offset this, but only to a point. If $200,000 isn’t collectable neither is $2,000,000 - interest theater, if you will.

My intuition is that higher education should be free at point of use, as lower education is, and that to a first order approximation we want to maximize the amount of it. I suspect the externalities created by a person learning something are strongly positive and much larger than the cost of teaching it to them or the amount of that value from knowing it that they personally would realistically be able to capture.

Some of this comes from improvements to coordination capacity. If, for example, everyone goes to college math class and learns linear algebra, then everyone gets some benefit from being able to use linear algebra, when they encounter a matching problem. But if everyone knows that everyone else knows linear algebra, then linear algebra gets to go into the pool of “common knowledge” that powers social coordination. The more we know we know, the more we can be on the same page.

Some of this also comes from specialization. Having people out there who have the knowledge and skills to do things I don’t is good for me in ways I am never actually going to pay them for. I might pay the salaries of, say, epidemiologists, through taxes, but I am never going to give them even a substantial fraction of the value I get from not dying constantly from infectious disease, so the amount available from their earnings to pay for their education is artificially low compared to how many of them we want.

Funding education with personal loans makes sense if education is meant to produce earners. But I see education as meant to produce people and societies. It is only at that level that the full benefit of education is seen, even for specialties that manage to capture a lot of value, and it is at that level that the benefits of, say, English majors are really delivered.

First best would be, anyone can walk into any college, sit down, and start learning stuff for free, with a framework of course requirements and degree granting to provide the gamification to encourage this, and with their needs for pedestrian things such as food, housing, and health care provided for. If that doesn’t produce enough education of the right types on its own, we might have to start paying people to go to school.

The loan forgiveness two-step is obviously much more complex, for no real benefit, so it’s strictly worse. But even to the extent that it’s just public spending on people who went to college, it seems better than not doing it. Especially if it changes behavior to result in more total education happening.

The degree to which it helps universities grow unboundedly wasteful is bad. But universities have already been growing almost unboundedly wasteful without the help of loan forgiveness, so if we really want to address that problem we need to redesign how they work, rather than just restricting the blood supply to the educational organ to starve the tumor. If we could actually put $200,000 worth of education into everyone’s head, and not just spend that while educating them, we’d be living in a paradise of abundant expertise.

What metrics do you think we could use to measure whether college education actually produces people and societies?

There’s a lot of money involved into spreading the meme that this is what happens but I haven’t seen any good evidence for that claim.

How do you know that English majors produce a lot of value for society?

On behalf of the Boomer generation I wish to offer my sincere apologies for how we totally ripped off our own children. We feasted on the big jobs in higher education, and sent you the bill.

I paid my own way through the last two years of a four year degree, ending in 1978. I graduated with $4,000 in debt. That could have been you too, but we Boomer administrators wanted the corner office.

I’ve spent my entire adult life living near, sometimes only blocks away, from the largest university in Florida. It used to be an institution of higher learning, but we Boomers turned it in to a country club. Very expensive. But no worries, cause we passed the bill on to you.

By the way, reading this post costs $1300. But don’t worry about it, because I can give you a loan, with interest of course.

Here is a Marginal Revolution writeup of the program:

The Student Loan Giveaway is Much Bigger Than You Think

The fundamental problem with student loans is that education is an intangible asset. Unlike a loan to buy a home or a car, there’s nothing that the lender can repossess if things go sideways. Financing education, both at the individual level and societal level, is always going to be a difficult problem, contentious and fraught. That being said, there’s some low hanging fruit.

1. Streamline the collection of student debt by creating a system of payroll deductions—maybe even add it to W4′s. It’s all going to the U.S. Treasury anyway.

2. Cap payments at a fixed percentage of the borrower’s federal tax liability, say 20%. Thus if you pay $10 in taxes in a given pay period, at most $2 would go toward your loan.

3. Prorate PSLF instead of making it all-or-nothing—if you work half a year for a qualifying employer, you’d get 5% of your principal written off.

4. Federal student loans are unique compared to other loans in that they’re completely forgiven when the borrower dies. That’s nice, but it also means that a significant portion of the high interest rates is likely due to default risk. Borrowers should be allowed to get a reduced rate if they buy credit life insurance, making the government (that is, the lender) the beneficiary.