I am posting this now largely because it is the right place to get in discussion of unrealized capital gains taxes and other campaign proposals, but also there is always plenty of other stuff going on. As always, remember that there are plenty of really stupid proposals always coming from all sides. I’m not spending as much time talking about why it’s awful to for example impose gigantic tariffs on everything, because if you are reading this I presume you already know.

The Biggest Economics Problem

The problem, perhaps, in a nutshell:

Tess: like 10% of people understand how markets work and about 10% deeply desire and believe in a future that’s drastically better than the present but you need both of these to do anything useful and they’re extremely anticorrelated so we’re probably all fucked.

In my world the two are correlated. If you care about improving the world, you invest in learning about markets. Alas, in most places, that is not true.

The problem, in a nutshell, attempt number two:

Robin Hanson: There are two key facts near this:

Government, law, and social norms in fact interfere greatly in many real markets.

Economists have many ways to understand “market failure” deviations from supply and demand, and the interventions that make sense for each such failure.

Economists’ big error is: claiming that fact #2 is the main explanation for fact #1. This strong impression is given by most introductory econ textbooks, and accompanying lectures, which are the main channels by which economists influence the world.

As a result, when considering actual interventions in markets, the first instinct of economists and their students is to search for nearby plausible market failures which might explain interventions there. Upon finding a match, they then typically quit and declare this as the best explanation of the actual interventions.

Yep. There are often market failures, and a lot of the time it will be very obvious why the government is intervening (e.g. ‘so people don’t steal other people’s stuff’) but if you see a government intervention that does not have an obvious explanation, your first thought should not be to assume the policy is there to sensibly correct a market failure.

No Good Very Bad Capital Gains Tax Proposals

Kamala Harris endorses Biden’s no-good-very-bad 44.6% capital gains tax rate proposal, including the cataclysmic 25% tax on unrealized capital gains, via confirming she supports all Biden budget proposals. Which is not the same as calling for it on the campaign trail, but is still support.

She later pared back the proposed topline rate to 33%, which is still a big jump, and I don’t see anything there about her pulling back on the unrealized capital gains tax.

Technically speaking, the proposal for those with a net worth over $100 million is an annual minimum 25% tax on your net annual income, realized and unrealized including the theoretical ‘value’ of fully illiquid assets, with taxes on unrealized gains counting as prepayments against future realized gains (including allowing refunds if you ultimately make less). Also, there is a ‘deferral’ option on your illiquid assets if you are insufficiently liquid, but that carries a ‘deferral charge’ up to 10%, which I presume will usually be correct to take given the cost of not compounding.

All of this seems like a huge unforced error, as the people who know how bad this is care quite a lot, offered without much consideration. It effectively invokes what I dub Deadpool’s Law, which to quote Cassandra Nova is: You don’t f***ing matter.

The most direct ‘you’ is a combination of anyone who cares about startups, successful private businesses or creation of value, and anyone with a rudimentary understanding of economics. The broader ‘you’ is, well, everyone and everything, since we all depend on the first two groups.

One might think that ‘private illiquid business’ is an edge case here. It’s not.

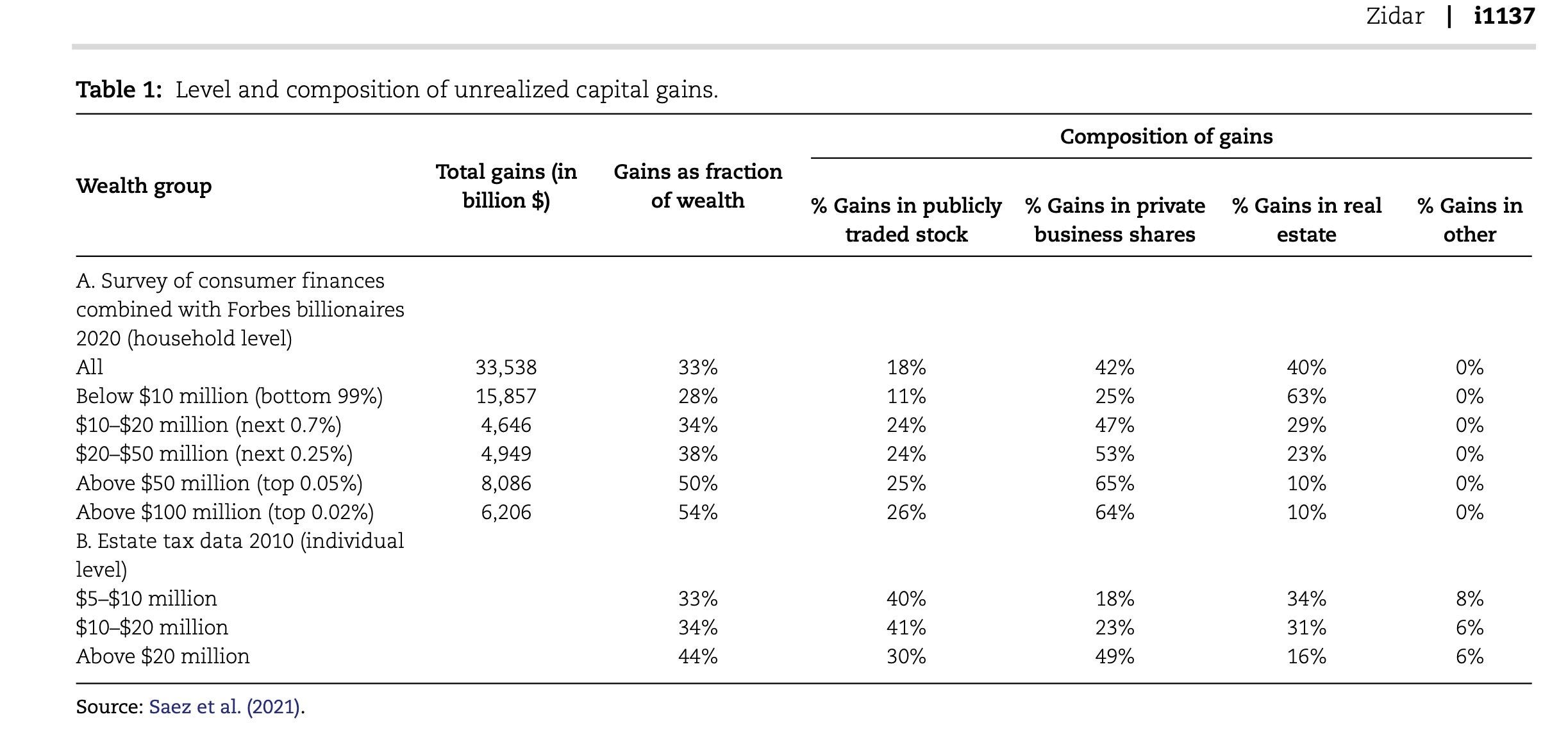

Owen Zidar: The discussions of unrealized capital gains for the very rich (ie those with wealth exceeding $100M) are often missing a key fact – two thirds of unrealized gains at the very top is from gains in private businesses (From SCF data)

When people discuss capital gains, they often evoke esoteric theories and think about simple assets like selling stock. They should really have ordinary private businesses in mind (like beverage distributors and car dealers) when thinking about these proposals at the top.

The share of transactions that stock sales represent has fallen substantially. It’s not about someone’s apple stock. We should be thinking about the decisions of private business owners when analyzing how behavior might respond to these policy changes.

As in, 64% of gains for those worth over $100m are in shares in private business, versus only 26% public stocks.

Here Dylan Matthews gives a steelman defense of the proposal. He says Silicon Valley is actually ‘exempt,’ so they should stop worrying, and their taxes can be deferred if over 80% of your assets are illiquid. That’s quite the conditional, there is an additional charge for doing it, there is very much a spot where you don’t cross 80% and also cannot reasonably pay the tax, if your illiquid assets then go to zero (as happens in startups) you could be screwed beyond words, and all the rates involved are outrageous beyond words, but yes it isn’t as bad as the headlines sound.

Roon: Probably not on board but it’s definitely clear sans behavioral econ stuff charging only at realization time causes pretty distorted incentives including eg holding onto windfall long after you think it’s stopped accumulating and thereby depriving new opportunities of capital.

Otoh this is caused untold gains for people who would’ve been too paperhands to hold otherwise.

Also untold unrealized gains that turned into losses. Easy come, easy go. Certainly the distortion here is massive. I do agree this is a problem. I like the realistic solutions even less, especially as they would effectively make it impossible for founders to maintain control.

Perhaps in some narrow circumstances there is something that could be done, and one could argue for taxing unrealized gains on some highly liquid and fungible investment types, so you avoid perverse outcomes including sabotage of value (e.g. in the hypothetical ‘harbinger tax’ world, you actively want to sabotage the resale value of everything you own that you want to actually use).

But would that come with a reduction in the headline rate? Here, clearly that is not the intention. So the compounding of the taxes every year would mean an insane effective tax rate, where you lose most of your gains, and in general capital would be taxed prohibitively. No good. Very bad.

And also of course if you tax liquidity you get a lot less liquidity. Already companies postpone going public a lot, we have private equity, and so on. You have lots of reasons to not want to be part of the market. What happens if you add to that bigly?

We should not be shocked that Silicon Valley talked about the consequences of a proposal while hallucinating a different proposal. They have a pattern of doing that. But it is not like the details added here solve the problem.

When you look at the details further, and start asking practical questions, as Tyler Cowen does here, you see how disastrously deep the problems go. Even in an ideal version of the policy, you are facing nightmare after nightmare starting with the accounting, massive distortion after distortion, you cripple innovation and business activity, and liquidity takes a massive hit. Tax planning becomes central to life, everything gets twisted and much value is intentionally destroyed or hidden, as with all Harbinger tax proposals. This is in the context of Tyler critiquing an attempted defense of the proposal by Jason Furman.

Jason Furman on Twitter says that his critiques are for a given overall level of taxation of capital gains. Arthur calls him out on the obvious, which is that we are not proposing to hold the overall level of taxation of capital gains constant, the headline rate is not coming down and thus if this passes the effective rate is going way, way up. And Harris proposes to raise the baseline rate to 44.6%.

Tyler Cowen successfully persuaded me the proposal is worse than I thought it was, which is impressive given how bad I already thought it to be.

Alex Tabarrok throws in the distortion that a lot of valuation of investments is a change in the discount rate. The stock price can and sometimes does double without expected returns changing. And he emphases Tyler’s point that divorcing the entrepreneur from his capital is terrible for productivity, and is likely to happen at exactly the worst time. Many have also added the obvious, which is that the entrepreneur and investors involved can backchain from that, so likely you never even reach that point, the company will often never be founded.

Here the CEO of Dune Analytics reports on the exodus of wealthy individuals that is Norway, including himself after he closed a Series B and was about to face an outright impossible tax bill.

The most ironic part of this is that the arguments for taxing unrealized capital gains are relatively strong among people with much lower net worths, if you could keep the overall level of capital taxation constant. You encourage someone like me to rebalance, and not to feel ‘locked into’ my portfolio, and my tax planning on those assets stops mattering. The need to diversify actually matters. Whereas it scarcely matters if people with over $100 million get to ‘diversify’ and indeed I hope they do not do so with most of their wealth.

Also a 44.6% capital gains tax, or even the reduced 33% later proposal, is disastrous enough on its own, on its face.

The good point Dylan makes here, in addition to ‘step-up on death is the no-brainer,’ is that currently capital gains taxes involve a huge distortion because you can indefinitely dodge them by not selling even fully liquid assets. I have a severely ‘unbalanced’ portfolio of assets for this reason, and even getting rid of the step-up on death would not change that in many cases.

The good news is I don’t see this actually happening. Neither do most others, for example here’s Brian Riedl pointing out this isn’t designed to be a real proposal, which is why they never vote on it.

The better news is that this could create momentum for the actually good proposals, like ending the capital gains step-up on death or taxing borrowing against appreciated stocks. I do think those wins could be a big deal.

The bad news is that the downside if it did happen is so so bad, and you can never be fully sure. The other bad news is that there are lots of other bad economic proposals, including Trump’s tariffs and Harris’s war on ‘price gouging,’ to worry about.

The more I think this, the issue is we fail to close other obvious tax loopholes that are used by the wealthy. In particular, borrowing against assets without paying capital gains, and especially doing this combined with the step-up of cost basis at death.

In today’s age of electronic records, asking that cost basis be tracked indefinitely for assets with substantial cost basis seems eminently reasonable.

So I see two potential compromises here, we can do either or both.

Backdate this responsibility to a fixed date, and say that you can choose the known true cost basis or the cost basis from a fixed date of let’s say 2010, whichever is higher, to not retroactively kill people without good records. If we want to exempt family farms up to some size limit or whatever special interests, sure, I don’t care.

Set a size limit. Your estate can only ‘step up’ the cost basis by some fixed amount, let’s say $10 million total. If you’re worth more than that, you’re worth enough to keep good records or pay up.

Then we can combine that with the obvious way to deal with loans against assets, which is to say for tax purposes that any loan on an asset that exceeds its cost basis is a realized capital gain (which also counts as a basis step-up). You just realized part of the gain. You have to pay taxes on that part of your gain now.

Tyler Cowen argues against this by noting that if the loan against an asset charges interest, you aren’t any wealthier from having access to it. Someone is loaning you that money for a reason. Except I would say, if you have a so-far untaxed asset worth $100, and you borrow $100 against it (yes obviously in real life you don’t get the full amount), you should be able to use appreciation of the asset to pay the interest on the borrowing, so you can indeed effectively spend down what you have earned, in expectation. So I see why people see this as evading a tax.

And we should also say that if you donate stocks or other appreciated assets, you can only claim the cost basis as a deduction unless you also pay the capital gains tax on the gain.

We might also have to do something regarding trust funds.

In exchange, lower the overall capital gains rate to keep total revenue constant.

Scott Sumner uses this opportunity to ask why we would even tax realized capital gains, with the original sin being taxing income rather than consumption. I strongly agree with him. Given that we are stuck with income taxes as a baseline, we should strive to minimize capital gains as a revenue source.

I’ll stop there rather than continue beating on the dead horse.

Hot Tip

We can now move on to talking about ordinary decent deeply stupid and destructive ideas, such as the Trump proposal, now copied by Harris, to not tax service tips.

Alex Tabarrok: If tip’s aren’t taxed, tips will increase, wages will fall, no increase in compensation.

The potential catch on total compensation is if the minimum wage binds. If tips are untaxed, the market wage for many jobs would presumably be actively negative. So even limiting it at $0 would cause an issue. That’s a relatively small issue.

The straightforward and obvious issue is this is stupid tax policy. Why should the waiter who lives off tips and earns more pay lower taxes than the cook in the back? This does not make any sense, on any level, other than political bribery.

Tyler Cowen tries to focus on the contradictory economic logic between tips and minimum wage. Either labor supply is elastic or inelastic, so either the minimum wage kills jobs or this new subsidy gets captured by employers in the form of lower wages. Unless, of course, this is illegal, via the minimum wage?

I see this as asking the wrong questions. You do not need to know the elasticity of labor supply to know not taxing tips is bad policy. No one involved is thinking in these economic terms, or cares. Bribery is bribery, pure and simple.

Also one can make a case that this will increase tipping. If people know tips are untaxed, then this is a reason to tip generously. Perhaps this increases total amount paid by consumers, so there is room for both employee and employer to benefit? But it would do so by being effectively inflationary, if this did not go along with lower base prices.

The bigger and more fun to think about issue is: What happens when there is a very strong incentive to classify as much of everyone’s income as possible as tips? What other jobs can qualify as offering ‘service tips’ versus not, and which can be used to effectively launder pay?

As an obvious example, a wide variety of sex workers can non-suspiciously be paid mostly in tips, and if elite can be paid vast amounts of money per hour, and it is definitely service work. Who is to say what happens there? What you’re into? Could be anything.

The case for not taxing tips is that if honest workers declare tips while dishonest workers are free not to and mostly suffer no consequences, what you are actually taxing is honesty and abiding by the law. I do find this unfortunate, and the de facto law here is to not report tips up to some murky threshold, and similar to the rule for gamblers, that if you want to conspicuously spend the money then you have to declare it. Alas, there are many such cases, where you need a law on the books to prevent rampant abuse.

Gouging at the Grocer

On the question of food and grocery prices, they aren’t even up in real terms.

Dean Baker: Contrary to what you read in the papers, food is not expensive. In the last decade, food prices have risen 27.3 percent, the overall inflation rate has been 32.0 percent. The average hourly wage has risen 43.3 percent.

Why weren’t reporters telling us about all the people who couldn’t afford food ten years ago?

Your periodic reminder that an hour of unskilled labor buys increasing amounts of higher quality food over time. Food prices are something people notice and feel. They look for the ones that go up, not the ones that go down. The fact that food is cheaper in real terms, and also better, is seemingly not going to change that.

I sympathize. It gets to me too, when I see the prices of staples like milk. Yet I also know that those additional costs are trivial, and that the time I spend to get good prices is either spent on principle, or time wasted.

I do not sympathize with those warning about ‘price gouging’ or attempting to impose anything remotely resembling price controls, especially on food. If this actually happens, the downside risk of shortages here should not be underestimated.

John Cochrane fully and correctly bites all the bullets and writes Praise for Price Gouging.

These two paragraphs are one attempt among many attempts to explain why letting prices adjust when demand rises is good, actually.

John Cochrane: But what about people who can’t “afford” $10 gas and just have to get, say, to work? Rule number one of economics is, don’t distort prices in order to transfer income. In the big scheme of things, even a month of having to pay $10 for gas is not a huge change in the distribution of lifetime resources available to people. “Afford” is a squishy concept. You say you can’t afford $100 to fill your tank. But if I offer to sell you a Porsche for $100 you might suddenly be able to “afford” it.

But more deeply, if distributional consequences of a shock are important, then hand out cash. So long as everyone faces the same prices. Give everyone $100 to “pay for gas.” But let them keep the $100 or spend it on something else if they look at the $10 price of gas and decide it’s worth inconvenient substitutes like car pooling, public transit, bicycles, nor not going, and using the money on something else instead.

The post contains many excellent arguments, yet I predict (as did others) this will persuade approximately zero people, the same way John failed to persuade his mother as described in the post. People simply don’t want to hear it.

Noncompetes Nonenforcement Cannot Compete With Courts

The FTC’s attempted ban on noncompetes is blocked nationwide for now, with the Fifth Circuit (drink?) setting it aside and holding it unlawful, that the FTC lacks the statutory authority. The FTC does quite obviously lack the statutory authority, and also as noted earlier IANAL and I doubt courts still think like this but to me this seems like a retroactive abrogation of contracts, and de facto a rather large taking without compensation in many cases, And That’s Terrible?

We Used to Be Poor

Your periodic reminder that no matter how much tough it might be today in various ways, we used to be poor, and work hard, and have little, and yes that kind of sucked.

Eric Nelson: These posts make me crazy. My father worked two jobs and my mother worked one to support 3 kids. We lived a life this woman would consider abuse now. Canned food, 1 TV, no microwave, no computers, no vacations, no air conditioning, beater cars, no dentist, no brand name anything.

In the mid80s, as a teen, I worked 365 days a year at 5am to make money so I could afford Converse sneakers, cassette tapes, and college applications.

Mark Miller tries to defend this as legit, saying that everyone clipped coupons and bought what was in season and bought their clothes all on sale and ate all their meals at home, but it was all on one income so it was great.

Even if that was typical, that sounds to me like one person earning income and two people working. Except the second person’s job was optimizing to save money, and doing various tasks we now get to largely outsource to either other people or technology. A lot of that saving money was navigating price discrimination schemes. All of it was extremely low effective wage for the extra non-job work. People went to extreme lengths, like yard sales, to raise even a little extra cash because they had no good way to use that time productively, and turn that time into money.

As usual, a lot of responses are not aware that home ownership rates are essentially unchanged, both overall and by generation by age, versus older statistics, and despite less children the new homes are bigger.

So, once again: We are vastly richer than we were. We consume vastly superior quality goods, in larger quantities, with more variety, even if you exclude pure technology and electronics (televisions, computers, phones and so on), including housing. An hour of work buys you vastly more of all that. Those who dispute this are flat out wrong.

The part I most appreciate: All things entertainment and information and communication, which are hugely important, are night and day different. You can access the world’s information for almost free. You can play the best games in history for almost free. You can watch infinite content for free. Those used to be damn expensive.

However, the ‘standard of living’ going up also means that what we consider the bare necessities, the things we must buy, have also gone way up. As Eric points out, we would not find what those ‘comfortable’ families of yesteryear had to be remotely acceptable, in any area.

In many cases, it would be illegal to offer something that shoddy, or be considered neglect to deny such goods. In others, you would simply be mocked and disheartened or be unable to properly function.

Then there are the things that actually did get vastly worse or more expensive. Housing (we end up with more anyway, because we pay the price), healthcare and education are vastly more expensive, and all mostly to stay in place. On top of that, various forms of social connection are much harder to get, friendship and community are in freefall and difficult to get even with great effort, atomization and loneliness are up, attention is down while addiction is up, dating is more toxic and difficult, people feel more constrained, freedom for children has collapsed, expectations for resources invested in children especially time is way up, and as a result of all that felt ability to raise children as a result of all of this is way down.

As a result, many people do find life tougher, and feel less able to accomplish reasonable life goals including having a family and children. And That’s Terrible. But we need to focus on the actual problems, not on an imagined idyllic past.

In particular, we need to be willing to let people live more like they did in the actual past, if they prefer to do that. Rather than rendering it illegal to live the way Eric Nelson grew up, we should enable and not look down upon living cheap and giving up many of the modern comforts if that is their best option.

Everywhere But in the Productivity Statistics

The Revolution of Rising Expectations, and the Revolution of Rising Requirements, are the key to understanding what has happened, and why people struggle so much.

Arnold Kling questions the productivity statistics, citing all the measurement problems, and notes that life in 2024 is dramatically better than 1974 in many ways. Yes, our physical stuff is dramatically better in ways people do not appreciate.

The big problem is that most of the examples here are also examples of new stuff that raises our expected standard of living. We went from torture root canals to painless root canals, that is great, so is the better food and entertainment and phones and so on, but that does not allow us to make ends meet or raise a family. Whereas other aspects that are not our ‘stuff’ have also gotten worse and more onerous, or more expensive, or we are forced to purchase a lot more of them.

I would definitely take 2024 over any previous time (at least ignoring AI existential risks), but the downsides are quite real. People miss something real, but they don’t know how to properly describe what they have lost, and glam onto a false image.

That’s why I emphasize the need to consider what an accurate ‘Cost of Thriving’ index would look like.

They Don’t Make ’Em Like They Used To

And that’s more often than not a good thing.

We instead get this persistent claim that ‘we don’t make things like we used to,’ that the older furniture and appliances were better and especially more durable. J.D. Vance is the latest to make such claims. Is it true?

Jeremy Horpedahl has some things to say about J.D.’s 40 year old fridge.

Jeremy Horpedahl: I don’t know anything about whether fridges of the past preserved lettuce longer, but let me tell you a few things about 40-year-old fridges in this here thread Most important point: fridges are *much cheaper* today. How much? Almost 5 times cheaper…

Let’s compare apples to apples as much as we can.

In 1984, you could buy a 25.7 cu foot side-by-side fridge/freezer with water/ice in the door for $1,359.99.

Today, you can get a similar model at Home Depot for $998

That’s right… it’s cheaper today in *nominal terms.*

But wages also increased since 1984, from about $8.50 to $30

So with the time it took to buy the 1984 fridge new, you could have to work about 160 hours.

With 160 hours of work today, you would earn $4,800, enough to buy almost FIVE FRIDGES today.

But wait, there’s more!

Sears estimated the annual cost to operate that fridge was $116.

Using the national average electricity price in 1984 (8.2 cents/kWh), it used about 1,415 kWh. To operate the 1984 fridge today (assuming no efficiency loss) would cost about $250/year.

But the 2024 fridge only uses about 647 kWh per year — only about 45% as much electricity (the improvement over 1970s fridges is even more dramatic). That will cost $115 today.

In other words, if you still have a 40-year old fridge, you could throw it out and buy a new one, and in about 7.5 years it will have paid for itself in lower energy costs (assuming current prices, but also assuming that 1984 fridge is still as efficient as it was new).

But wait, you might ask, will that new fridge even last 7.5 years? Doesn’t stuff wear out faster today? Data is a little harder to find (anecdotes are easy to find!), but using the Residential Energy Consumption Survey we can see this is a bit overstated.

…

The oldest cutoff is 20 years. In 1990, just 8.4% of households used a fridge that was 20 years or older. In 2020, this was slightly lower: 5.5%.

But 20 year fridges were never common 10 years or older? Again a decline, from 38.2% to 35.1% — but not dramatically different.

…

It’s fine if J.D. Vance enjoys his 1984 fridge, but this doesn’t mean “economics is fake.”

…

Bottom line on this question: if you were offered a $5,000 fridge, costing $250 per year in electricity to operate, keeping vegetables fresh slightly longer (4 weeks instead of 3), but it was guaranteed to last 50 years, would you buy it?

There are many valid complaints about 2024. Our appliances are not one of them.

Furniture might be one area where the old stuff is competitive, but my guess is this is also a failure to account for real prices, or how much we actually (don’t) value durability.

Disclosure of Wages Causes Lower Wages

Another study finds that public disclosure of wages causes wage suppression.

Abstract (Junyoung Jeong): This study examines whether wage disclosure assists employers in suppressing wages.

…

These findings suggest that wage disclosure enables employers in concentrated markets to tacitly coordinate and suppress wages.

I continue to think this gets the mechanism wrong. Wage disclosure does not primarily assist employers in suppressing wages. What it primarily does, as I’ve discussed before, is give employers much stronger incentive to suppress wages. Everyone is constantly comparing their salary to the salary of others, and comparing that to the status hierarchy (or sometimes to productivity or market value or seniority or what not).

Thus, before, it often would make sense to pay someone more because they were worth the money, or because they had other offers, or they negotiated hard. Now, if you do that, everyone else will get mad, treat that as a status and productivity claim, and also use that information against you. This hits especially hard when you have a 10x programmer or other similarly valuable employee. People won’t accept them getting what they are worth.

I first encountered this watching the old show L.A. Law. One prospective associate asks for more money than is typical. He’s Worth It, so they want to give it to him, but they worry about what would happen if the other more senior associates found out, as they’d either have to match the raise, or the contradiction between wages and social hierarchy would cause a rebellion.

Exactly. It is because wage disclosure allows comparison and coordination on wages, and allows employees to complain when they are treated ‘unfairly,’ that it ends up raising the cost of offering higher wages, thus suppressing them. Chalk up one more for ‘you can make people better off on average, or you can make things look fair.’

In Other Economic News

Due to a combination of factors but it is claimed primarily due to unions, it costs about five times as much to put the same show on in New York as it does in London, with exactly the same cast and set. It is amazing that such additional costs (however they arise) can be overcome and we still put on lots of shows here.

National industrial concentration is up, in the sense that within industry concentration is up, but the shift from manufacturing to services means that local employment concentration is down. I notice I don’t know why we should care, exactly?

The 2002 Bush steel tariffs cost more jobs due to high steel prices than they protected, including losing jobs in steel processing. Long term, it makes the whole industry uncompetitive as well, same as our shipbuilding under the Jones Act.

Department of Justice lawsuits for alleged fraud in FHA mortgages caused 20% reduction in subsequent FHA mortgage lending in the area, concentrated on the heavily litigated against banks. Demand, meet supply. What else would you expect? The banks are acting rationally, if you wanted the banks to issue mortgages to poor people you wouldn’t sue them for doing that.

SwiftOnSecurity thread about people’s delusions about car insurance, thinking it is a magical incantation that fixes what is wrong rather than a commercial product. Patrick McKenzie has additional thoughts about how to deal with such delusions as a customer service department.

Tyler Cowen talks eight things Republicans get wrong about free trade. He is of course right about all of them. It is especially dismaying that we might get highly destructive tariffs soon, especially on intermediate goods. On the margin shouting into the void like this can only be helpful.

New study on changes in entrepreneurship on online platforms like Shopify, with minority and female entrepreneurs especially appreciating the support such platforms bring despite the associated costs. A lot of businesses saw strong growth.

A challenge: Does it ‘conserve resources’ if the conserved resources fall into the hands of someone who would waste them? There are of course

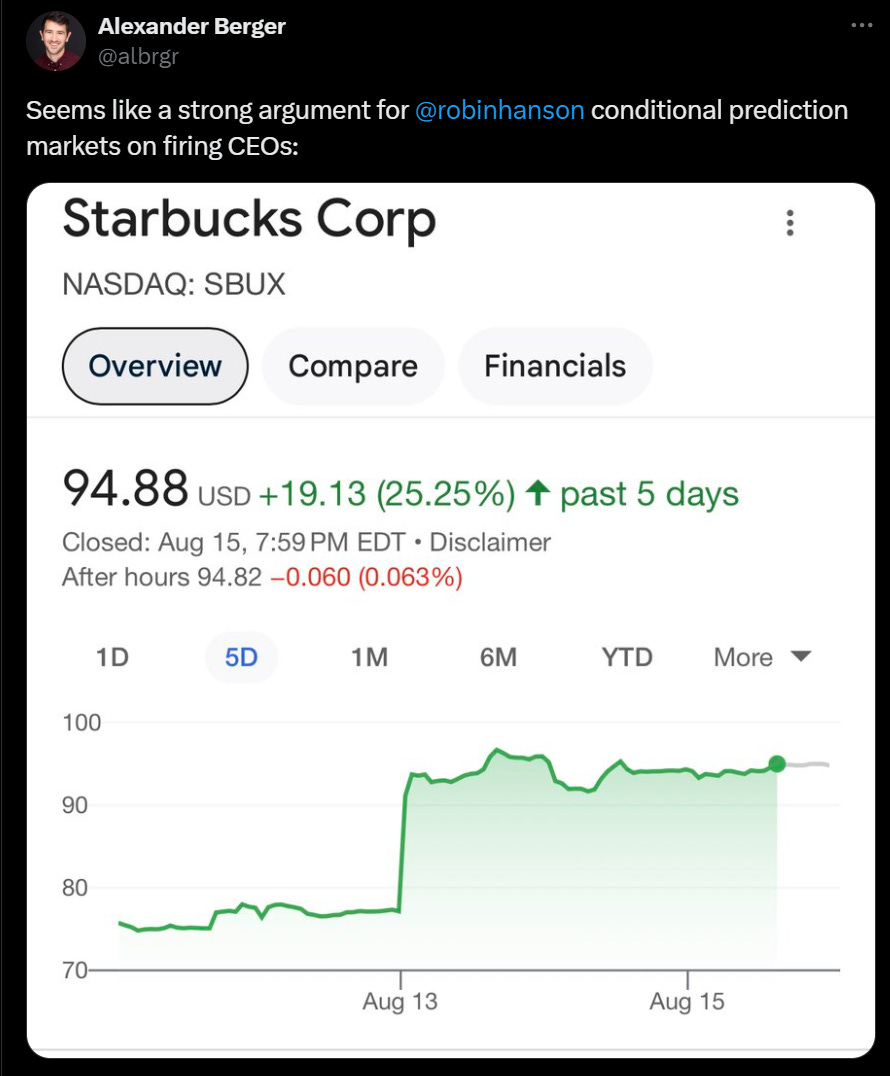

Market to fire the CEO you say?

It is not a strong as it looks, because in this case everyone knew to fire the CEO. I knew the market wanted this CEO fired, and I don’t care at all. Still, a strong case.

New York City’s biggest taxi insurer, insuring 60% of taxis including rideshare vehicles, is insolvent, risking a crisis. Other than ‘liabilities exceeding premiums’ the article doesn’t explain how this happened? Medallion values crashed but that was a while ago and shouldn’t be causing this. They worry that ‘drivers will face increased premiums’ but if the insurer offering current premiums is now insolvent, presumably they were indeed not charging enough.

What, me leave California because they tax me over 10% of my gross income?

Roon: the only reason to leave California for tax reasons is if you believe you’ve made most of the money you’ll ever make in the past.

Which is fine but there’s a vaguely giving up vibe to it.

So first off, yeah, can’t leave, the vibes would be off. Classic California.

Second, obviously there are other good reasons to want to live somewhere else, and 10%+ of gross income is a huge cost, especially if you do plan to earn a lot more. Of course it is a good reason to leave. Roon is essentially assuming that one can only make money in California, that it would obviously be a much bigger hit than 10% (really 15%+ given other taxes) to be somewhere else. Why assume that? Especially since most people do not work in AI.

The Efficient Market Hypothesis is (Even More) False

The Less-Efficient Market Hypothesis, a paper by Clifford Asness.

Abstract: Market efficiency is a central issue in asset pricing and investment management, but while the level of efficiency is often debated, changes in that level are relatively absent from the discussion.

I argue that over the past 30+ years markets have become less informationally efficient in the relative pricing of common stocks, particularly over medium horizons.

I offer three hypotheses for why this has occurred, arguing that technologies such as social media are likely the biggest culprit.

Looking ahead, investors willing to take the other side of these inefficiencies should rationally be rewarded with higher expected returns, but also greater risks. I conclude with some ideas to make rational, diversifying strategies easier to stick with amid a less-efficient market.

The Efficient Market Hypothesis is Now More False. I find the evidence here for less efficient markets unconvincing. I do suspect that markets are indeed less long-term efficient, for other reasons, including ‘the reaction to AI does not make sense’ and also the whole meme stock craze.

What would be the point of not realizing gains indefinitely if we got rid of the step-on on death?

The usual reason is compounding. If you have an asset that is growing over time, paying taxes from it means not only do you have less of it now, but the amount you pulled out now won’t compound indefinitely into the future. You want to compound growth for as long as possible on as much capital as possible. If you could diversify without paying capital gains you would, but since the choice is something like, get gains on $100 in this one stock, or get gains on $70 in this diversified basket of stocks, you might stay with the concentrated position even if you would prefer to be diversified.

“harberger tax,” for anyone trying to look that up.

Those seem contradictory, would you mind elaborating?

Scenario: you have equity worth (say) $100 million in expectation, but of no realized value at the moment.

You are forced to pay unrealized gains tax on that amount, and so are now $25 million in the hole. Even if you avoid this crashing you immediately (such as by getting a loan), if your equity goes to $0 you’re still out for the $25 million you paid, with no assets to back it.

The fact that this could be counted as a prepayment for a hypothetical later unrealized gain doesn’t help you, you can’t actually get your money back.

But the OP explicitly said (as quoted in the parent) that the proposal allows for refunds if the basis is not (fully) realized, which would cover the situation you’re describing.

Somehow I missed that bit.

That makes the situation better, but there’s still some issue. The refund is not earning interest, but you liabilities are.

Take the situation with owing $25 million. Say that there’s a one year time between the tax being assessed and your asset going to $0 (at which time you claim the refund). In this time the $25 million loan you took is accruing interest. Let’s say it does so at a 4% rate per year, when you get your $25 million refund you therefore have $26 million in loans.

So you still end up $1 million in debt due to “gains” that you were never able to realize.

That’d be a problem indeed, but only because the contract you’re proposing is suboptimal. Given that the principal is fully guaranteed, it shouldn’t be terribly difficult for you to borrow at >4% yearly with a contingency clause that you don’t pay interest if the asset goes to ~0.

Showerheads are worse now. They don’t make ’em like they used to because of restrictions on flow rate. Trump was absolutely right to complain about it. Delenda EPA.

Sure, but do you believe this particular proposal is unusual in appealing to one group at the expense of another? It is my understanding that this is how campaigning for election generally works.