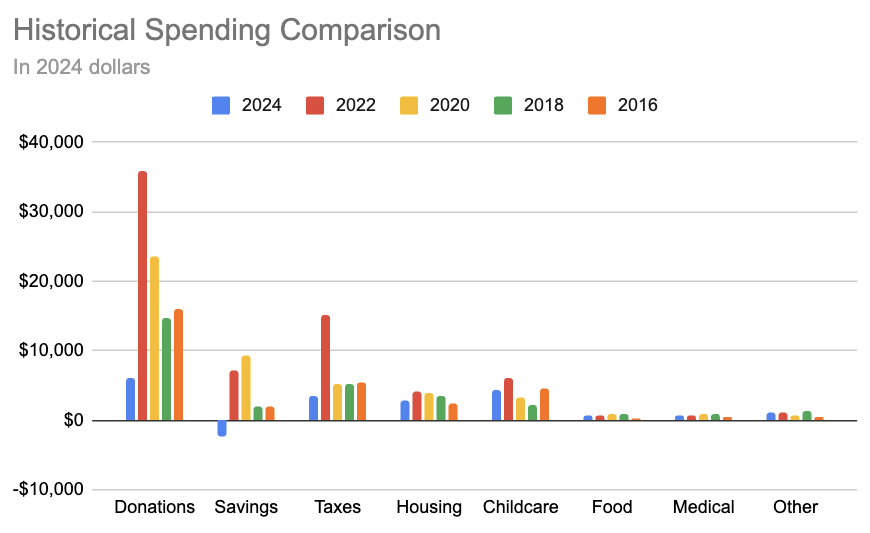

Julia recently posted about how we’re still donating 50%, which included this chart of monthly spending from our 2024 spending update:

While each year before 2024 we’d been saving some, 2024 was the first year in which we were drawing from savings to make donations. Noticing this prompted David Denkenberger to ask:

If you don’t mind me asking, how does the return on your investments factor in? E.g., is the negative savings offset by return such that your net worth is not falling?

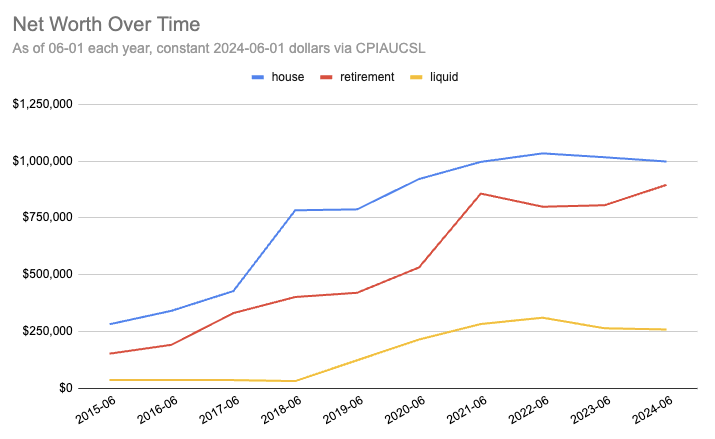

This is a good question! Our net worth hasn’t been something I’ve been regularly calculating, but this seemed like a good opportunity to figure out how it’s changed over time.

Things I counted:

Liquid: cash in our bank account, stocks we own in a standard investment account.

Retirement: 401k, HSA

House: value of the house according to Zillow, less loan balance

Things I didn’t count:

Credit card balances (we pay these off in full each month)

The value of our other stuff, which has been going up a bit over time. The biggest single possession is probably our half of the shared car (~$2.9k), followed by my mandolin (~$2k). A full accounting here would be a ton of work.

The value of my 7,049 options for Wave and 56 shares of Zepz, from when I was laid off from Wave. I have no idea how much these are worth.

Human and social capital.

While I would have liked to go back to ~2008 when we had essentially zero net worth, since I haven’t been tracking this I was reliant on the records various providers keep, which seem to go back ten years. I took values as of June 1st each year when possible, because right around the end of the year there’s a lot of variability due to when donation related transactions hit our bank account. In cases where I could only get January 1st numbers I interpolated to get a June 1st number. I adjusted for inflation using the CPIAUCSL, so I could do this in constant 2024-06-01 dollars.

Here’s the chart:

The biggest factor is appreciation on our house (which is bad), followed by the stock market doing well (which is good).

To answer David’s question, it looks like our net worth hasn’t been going down as we draw from savings. This seems like more reason to continue donating half, and not to respond to our now-lower income by donating a smaller fraction.

(I continue to be quite unsure how to think about saving for retirement and kids college.)

I’m glad my suggestion was helpful!

In normal worlds, I think you are in excellent shape, with how your greater than $2 million net worth compares to median of around $100,000 and mean of around $800,000 net worth for households in their 40s in the US. Also, I think you have greater net worth than more than 99% of households in the world. If you let your taxable account go to zero, then you would likely have to pay less for college, because often the retirement accounts are not included in those calculations. If you didn’t add anything more to your retirement account and it just grew 8% per year for twenty years, you would have ~$4 million. Then with the rule of thumb of drawing 4% per year during retirement, you would have an annual income of ~$160k. And that would not be counting any Social Security, income from home downsizing, inheritance, etc.

As for AGI worlds, as many have pointed out, we could be all dead or all rich, so it wouldn’t matter. One person pointed out that wealth at the singularity might allow you to buy galaxies, but at least if you’re altruistic, the impact of reducing existential risk is many orders of magnitude greater. Others have pointed out that even if humanity on average is rich, there may not be UBI. As long as one has significant net worth, this should grow at least initially, and then the cost of living should fall, so you should be fine. However, for people without any net worth, especially outside countries that benefit a lot from AI, there is reason to be worried. I personally think that even if there is not universal UBI, the rich of the world would not allow the poor to starve en masse. But if you want to do better than just not starving, then having a modest amount of net worth I think is quite prudent.