Industry Matters 2: Partial Retraction

Epistemic status: still tentative

Some useful comments on the last post on manufacturing have convinced me of some weaknesses in my argument.

First of all, I think I was wrong that most manufacturing job loss is due to trade. There are several economic analyses, using different methods, that come to the conclusion that a minority of manufacturing jobs are lost to trade, with most of the remainder lost to labor productivity increases.

Second of all, I want to refine my argument about productivity.

Labor productivity and multifactor productivity in manufacturing, as well as output, have grown steadily throughout the 20th century, and continue to grow today. The claim “we are making more things than ever before in America” is true.

It’s also true that manufacturing employment has dropped slowly through the 70’s and 80’s until today. This is plausibly due to improvements in labor productivity.

However, the striking, very rapid decline of manufacturing employment post-2000, in which half of all manufacturing jobs were lost in fifteen years, looks like a different phenomenon. And it does correspond temporally to a drop in output and productivity growth. It also corresponds temporally to the establishment of normal trade relations with China, and there is more detailed evidence that there’s a causal link between job loss and competition with China.

My current belief is that the long-term secular decline in manufacturing employment is probably just due to the standard phenomenon where better efficiency leads to employing fewer workers in a field, the same reason that there are fewer farmers than there used to be.

However, something weird seems to have happened in 2000, something that hurt productivity. It might be trade. It might be some kind of “stickiness” effect where external shocks are hard to recover from, because there’s a lot of interdependence in industry, and if you lose one firm you might lose the whole ecosystem. It might be some completely different thing. But I believe that there is a post-2000 phenomenon which is not adequately explained by just “higher productivity causes job loss.”

Most manufacturing job loss is due to productivity; only a minority is due to trade

David Autor‘s economic analysis concluded that trade with China contributed 16% of the US manufacturing employment decline between 1990 and 2000, 26% of the decline between 2000 and 2007, and 21% over the full period. He came to this conclusion by looking at particular manufacturing regions in the US, looking at their exposure to Chinese imports in the local industry, and seeing how much employment declined post-2000. Regions with more import exposure had higher job loss.

Researchers at Ball State University also concluded that trade was responsible for a minority of manufacturing job loss during the period 2000-2010: 13.4% due to trade, and 87.8% due to manufacturing productivity. This was calculated using import numbers and productivity numbers from the U.S. Census and the Bureau of Labor Statistics, under the simple model that the change in employment is a linear combination of the change in domestic consumption, the change in imports, the change in exports, and the change in labor productivity.

Josh Bivens of the Economic Policy Institute, using the same model as the Ball State economists, computes that imports were responsible for 21.15% of job losses between 2000 and 2003, while productivity growth was responsible for 84.32%.

Justin Pierce and Peter Schott of the Federal Reserve Board observe that industries where the 2000 normalization of trade relations with China would have increased imports the most were those that had the most job loss. Comparing job loss in above-median impact-from-China industries vs. below-median impact-from-China industries, the difference in job loss accounts for about 29% of the drop in manufacturing employment from 2000 to 2006.

I wasn’t able to find any economic analyses that argued that trade was responsible for a majority of manufacturing job losses. It seems safe to conclude that most manufacturing job loss is due to productivity gains, not trade.

It’s also worth noting that NAFTA doesn’t seem to have cost manufacturing jobs at all.

Productivity and output are growing, but have slowed since 2000.

Real output in manufacturing is growing, and has been since the 1980’s, but there are some signs of a slowdown.

Researchers at the Economic Policy Institute claim that slowing manufacturing productivity and output growth around 2000 led to the sharp drop in employment. If real value added in manufacturing had continued growing at the rate it had been in 2000, it would be 1.4x as high today.

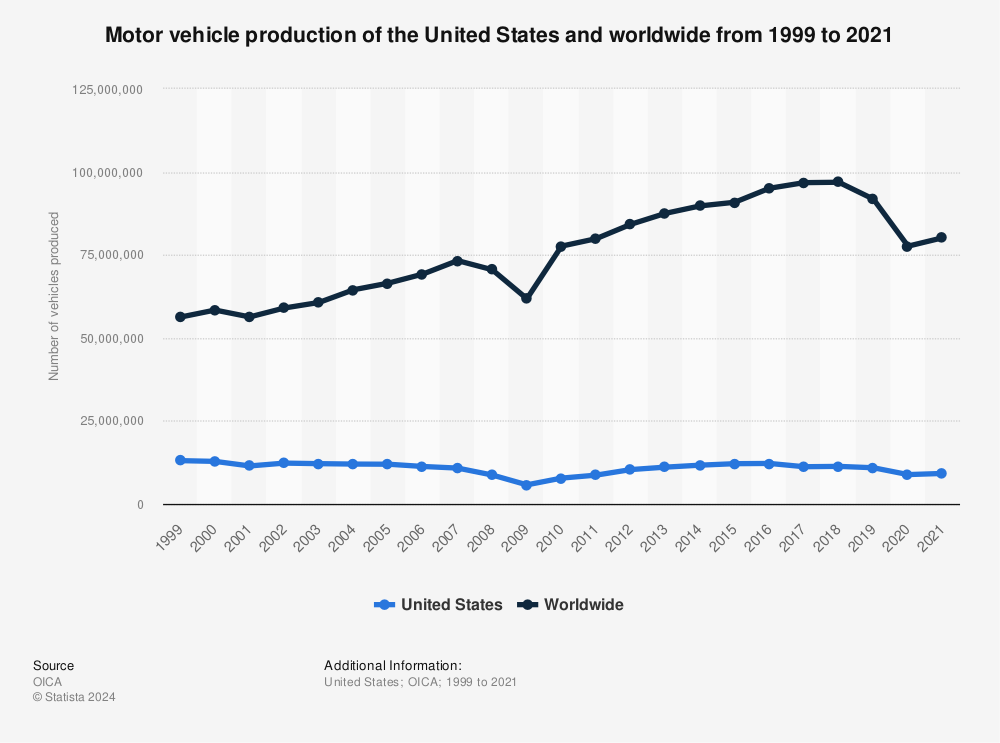

Manufacturing output aside from computers and electronic products has beenslow-growing since the 90’s. The average annual output growth rate, 1997-2015, in manufacturing, was 12% in computers, but under 4% in all other manufacturing sectors. (The next best was motor vehicles, at 3% output growth rate.)

US motor vehicle production has been growing far more slowly than global motor vehicle production.

{kind=link}

Here are some BLS numbers on output in selected manufacturing industries:

- steel mills: total value is 2.5x its 1987 value

basic chemical manufacturing: total value has quadrupled since 1987

- automobiles: total value has doubled since 1987

- airplanes: total value is 2.7x its 1987 value

- auto parts: total value is 2.5x its 1987 value

Semiconductors have actually not grown that much since 1995, but current value is still about double its 1987 value

As an average over the time period, this growth rate represents about 2.5%-3.5% annual growth, which is roughly in line with GDP growth. So manufacturing output growth averaged since the late 80’s isn’t unusually bad.

Labor productivity has also been rising in various industries:

- chemicals

- glass

- plastics

- forging and stamping

- petroleum and coal products manufacturing

- paper manufacturing

- wood product manufacturing

However, when we look at the first and second derivatives of output and productivity, the picture looks worse.

Multifactor productivity seems to have flattened in the mid-2000’s, and multifactor productivity growth has dropped sharply.

Manufacturing labor productivity growth is positive, but lower than it’s been historically, at about 0.45% in 2014, and a 4-year moving average of 2.1%, compared to 3-4% growth in the 90’s.

Multifactor productivity in durable goods is down in absolute terms since about 2000 and hasn’t fully recovered.

(Multifactor productivity refers to the returns to labor and capital. If multifactor productivity isn’t growing, then while we may be investing in more capital, it’s not necessarily better capital.)

Labor productivity growth in electronics is dropping and has just become negative.

Labor productivity growth in the auto industry is staying flat at about 2%.

Manufacturing output growth has dropped very recently, post-recession, to about 0. From the 80’s to the present, it was about steady, at roughly 1%. By contrast, global manufacturing growth is much higher: 6.5% in China, 1.9% globally. And US GDP growth is about 2.5% on average.

In some industries, like auto parts and textiles, raw output has dropped since 2000. (Although, arguably, these are lower-value industries and the US is moving up the value chain.)

Looking back even farther, there is a slowdown in multifactor productivity growth in manufacturing, beginning in the early 70’s. Multifactor productivity grew by 1.5% annually from 1949-1973, and only by 0.3% in 1973-1983. Multifactor productivity today isn’t unprecedentedly low, but it’s dropping to the levels of stagnation we saw in the 1970’s.

Basically, recent labor productivity is positive but not growing and in some cases dropping; output is growing slower than GDP; and multifactor productivity is dropping. This points to there being something to worry about.

What might be going on?

Economist Jared Bernstein argues that automation doesn’t explain the whole story of manufacturing job loss. If you exclude the computer industry, manufacturing output is only about 8% higher than it was in 1997, and lowerthan it was before the Great Recession. The growth in manufacturing output has been “anemic.” He says that factory closures have large spillover effects. Shocks like the rise of China, or a global glut of steel in the 1980’s, lead to US factory closures; and then when demand recovers, the US industries don’t.

This model also fits with the fact that proximity matters a lot. It’s valuable, for knowledge-transfer reasons, to build factories near suppliers. So if parts manufacturing moves overseas, the factories that assemble those parts are likely to relocate as well. It’s also valuable, due to shipping costs, to locate manufacturing near to expensive-to-ship materials like steel or petroleum. And, also as a result of shipping costs, it’s valuable to locate manufacturing in places with good transportation infrastructure. So there can be stickiness/spillover effects, where, once global trade makes it cheaper to make parts and raw materials in China, there’s incentives pushing higher-value manufacturing to relocate there as well.

It doesn’t seem to be entirely coincidence that the productivity slowdown coincided with the opening of trade with China. The industries where employment dropped most after 2000 were those where the risk of tariffs on Chinese goods dropped the most.

However, this story is still consistent with the true claim that most lost manufacturing jobs are lost to productivity, not trade. Multifactor productivity may be down and output and labor productivity may be slowing, but output is still growing, and that growth is still big enough to drive most job loss.

Crossposted from my blog: https://srconstantin.wordpress.com/2016/11/23/industry-matters-2-partial-retraction/

The argument that opening up trade relations with China shifted a bunch of manufacturing there seems pretty plausible. I’m not sure why this isn’t consistent with a story where the US is moving up the value chain, especially given that most growth seems to be coming from high-tech manufacturing.

I’m not sure how to interpret the slowed productivity growth. Naively, it seems like evidence against this explanation (if the US loses less capital-intensive manufacturing first). We should expect that if the least productive US firms exit due to Chinese competition, average productivity should go up because of this.

On the other hand I can make up explanations where we should expect this to cause slower measured productivity growth. Lower prices mean lower output (when measured in market value) and thus lower measured productivity, all else equal, so new competition from China could lower measured US productivity growth even if output measured in widgets produced per unit of labor or capital invested stays the same. If US manufacturers are slow to exit, this can lead to slowed productivity growth, as the incentive to raise output via investing in process improvements or new equipment declines in relevant areas of manufacturing.

My argument had been that if we were moving up the value chain successfully we’d see higher productivity, and we don’t.

My intuition is that something to do with knowledge/skill/synergy goes away if you move too much manufacturing away, which makes the manufacturing that remains less productive. For example, there are efficiency gains from having factories close to suppliers; if the parts manufacturers move to China, then the auto manufacturers in the US don’t get to have the same tight feedback loops with them, and so become less productive per worker and per dollar of capital, because the benefits of proximity don’t show up in either of those categories.

In autos, at least, we look worse when you measure “number of widgets” than when you measure dollar value. The total number of cars produced in the US has actually decreased. The peak was in 1978.

(I seem to recall that the US boosted sales by switching to SUVs, which were more expensive per unit.)